A classic example of why iBuying real estate doesn’t work.

Summary

This 6-unit property was in a prime area right next to Fulton Market. The apartment was listed at a relatively cheap $989k. According to the seller’s basic apartment info, such as bedroom count, the total potential rent for these apartments could have been $11,350 per month based on average comparable rentals, assuming we spent $30k-50k to update kitchens based on the pictures provided beforehand.

However, upon doing an in-person tour, we discovered that 2 of the 2-bedroom units would only be rentable as 1-bedroom + office units and most other units were undersized, bringing down the total income potential dramatically. In addition, the property was more of a distressed condition than the pictures indicated, requiring $100k+ to bring the property and its units up to those enhanced rent prices. Ultimately, the investment required would not yield the desired returns I’m looking for.

Final Outcome = No Offer Submitted.

Initial Evaluation

I’ve analyzed so many properties at this point, that it’s very easy for me to narrow down publicly listed properties that I’m interested in. 90% of properties that go on the market get ruled out immediately. After my initial filters, I put together a basic pros & cons list to see if I’m interested in doing an actual financial analysis. Of course, the pros & cons list will be riddled with assumptions that needed to be validated by an in-person tour, but it gives me enough filter out 50% of those that still remain.

Initial Pros & Cons

Pros:

- Prime location in West Town

- Current rents well under market comparables

- Value-add opportunity based on pictures provided

- Reasonable $989k listing price with under $170k per unit

- No lawncare required since no lawn in front or back

Cons:

- Property split into 2 buildings: 4 units in the brick building in front with 2 units in a coach house in the back.

- i.e. 2 roofs, 2 foundations, 2 xyz to manage

- No central AC

- This is a requirement in this neighborhood for ideal rent prices

- No parking (because coach house took up that space)

- Current owner has had the property for 50+ years

- This typically means that the property has never been renovated during ownership and requires lots of work

Open Questions:

- Are my target rents achievable with $30-50k CapEx investment?

- Can unfinished basement be converted into additional livable units?

- If so, that would immediately add $200k+ in asset value

- Are there any other major issues with the property?

It wasn’t completely obvious whether this would be a good investment or not, but the best investments are never obvious.

Revenue Growth Projections

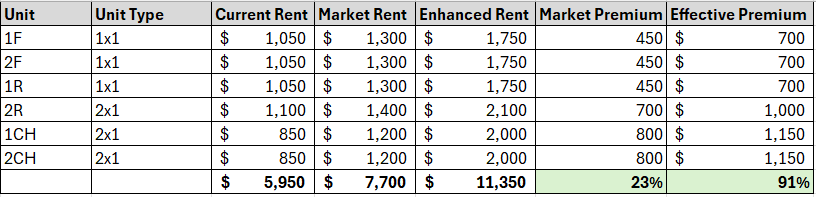

Typically, my first step for all value-add investment properties, I need to see how much of the top line revenue can be grown by either bringing rents up to market rate in their current condition and/or what the rents could be if enhancements are made to the apartments. In this case, based on the limited information of the unit types (bedroom and bathroom count), location, and provided pictures, I determined that the rent could be raised 23% with no extra work. This is very common. However, looking at the rents we could achieve with an average or above average apartment with the provided room counts were mindboggling.

The apartments could’ve achieved almost double the current rent.

Operating Expense Projections

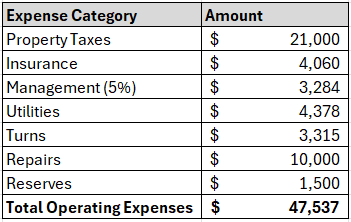

Expenses are the hardest to evaluate virtually, primarily because the information provided by the seller is either incomplete, misleading, or not applicable. A prime example are property taxes, where sellers utilize their property taxes, which are likely taxed based on the price they purchased at a long time ago and not what they are selling for. In some cases, these sellers are paying 1/3 of the taxes that will be incurred by the buyer. Thankfully, property taxes and rates are publicly available and can be roughly projected.

I also have some rules of thumb on maintenance and major project costs that I can use based on my existing portfolio and market averages I see through my work in the real estate tech industry. However, the reality is that without an in-person visit, these expense projections are just projections based on incomplete info. I only put the time in here to make sure it’s worth going out and spending an hour visiting a property and doing further analysis.

The annual operating expenses were estimated at $48,000, which is a very attractive amount if correct.

Investment Analysis

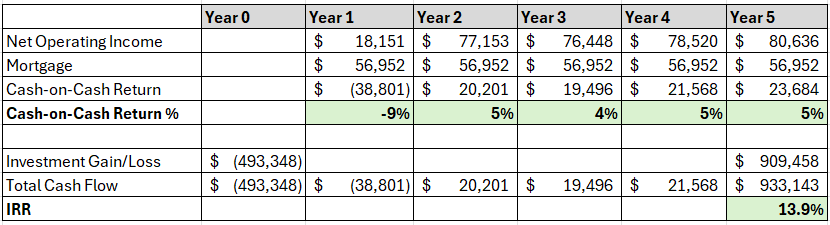

The assumed lifecycle of this investment, like most of my investments, is 5 years. Assuming we purchased this property for $989k, renovated it, and sold with a valuation was based on the cap rate, we could sell this property for over $1.6 million 5 years later. If that sounds too good to be true, just know that 70% of similar properties that are selling right now are listed above $1.6 million and they certainly have not been renovated recently.

In order to do those renovations, I assumed $10k needed per unit for a total of $60k upfront investment to bring these apartments up to market rent. The majority of this cost would be to install central AC & renovate the kitchens of all units. This is in addition to the upfront 30% down payment as well as financing fees and operating funds. We also assumed a mortgage with a 7.2% interest rate.

Projected annul cash-on-cash return is 5% with a 14% rate of return after 5 years!

Property Visit

Exterior

Driving up to the property, the neighborhood was just as I expected – classic Chicago brick buildings from the early 1900s, with trees overhanging the streets filled with cars. Around the corner was a magnet school, a premium in Chicago, which is incredibly desirable when compared to traditional Chicago public schools. There was also a lot of diagonal parking that took advantage of Ohio St., which was wider than most residential streets. This means more parking for residents, which is very desirable for tenants.

We first checked out the apartments in the front brick building. Before going inside, we could tell that there were some patches in the brick that required tuckpointing and the stairs throughout were incredibly old even for Chicago standards.

Main Building Apartments

With properties with multiple apartments, it’s very rare to be able to see all of the units so you have to make a few assumptions based on the properties shown and good questions to the seller’s agent. We were able to see 4 of the 6 units, and according to the seller’s agent, the other 2 units were identical in floor plan and condition to ones that we were able to see.

We weren’t too surprised by the small size of the apartments, bedrooms and the lack of bedroom closets since that was pretty clear from the online pictures we saw beforehand. As a positive surprise, the bathrooms were in better condition than what we assumed them to be.

Overall, the 4 apartments in the front were exactly what we were expecting.

Main Building Basement

Next, we went to the basement, which we knew would make or break the investment. The moment we got downstairs, we smelled a bit of sewage smell and/or general mustiness. On visual inspection, everything seemed fine though. However, there was a small humidifier which is a giveaway for the existence of water in some form. If that was the only issue, that’s something we could overlook, but it went downhill quickly.

The biggest question we had was whether or not we could convert the basement into a garden unit, which is very common in Chicago. Garden units don’t command the most rent, but a 2bed/1bath garden unit would easily add $200k+ to the resale value. Chicago has a very strict criteria for converting garden units, and the minimum height required is 7 feet. Unfortunately, the height was not big enough, so this was essentially a no-go.

As we continued through the basement, we also discovered that there were only 2 water heaters for the 4 units in the building, and only 3 gas meters (5 would be the correct amount of gas meters). My guess is that back in the day, the front 4-unit building was actually only a 2-unit building with a top floor and a bottom floor. That would make sense with the water heater and gas meter count, as well as why the units were so small.

There were also only 1 washer and dryer that only one of the residents used. In-unit laundry is ideal for premium rent, with shared in-building laundry required as a bare minimum. Not the end of the world with the current setup, but certainly another negative mark on the property that in-unit laundry could never really be done with the space and layouts of the individual apartments.

The poor condition of the basement had us really close to concluding this was not a good investment opportunity.

Coach House

A coach house is a smaller building in the back of the property. They are no longer permitted to be built, but many older Chicago properties have these 2nd buildings from many decades ago. When I first moved to Chicago, I lived in a 1 bedroom apartment in a coach house. They are certainly not built to the quality of a standard brick building, but they can provide for a solid income for property owners.

This coach house was on the bigger side, with two apartments claiming to have 2 bedrooms. There was a solidly built external staircase, and also a basement underneath the 2 units. The basement was extremely cluttered, and it was a step down from the outside, which is always a risk factor for water to get inside. Technically the ceiling was high enough to put a 3rd unit in the basement, but would be very costly and likely not get an acceptable rent amount.

The biggest issue with the coach house was simply that the apartments’ 2nd bedroom was way too small to really be classified as a 2nd bedroom. In reality, it was more like an office / den, and would lower the premium rent that I had projected before visiting the property.

At this point, I was 90% sure this would not be a viable investment that met my ROI targets.

Final Analysis

The financial analysis can be simply broken down into 3 parts: stabilized revenue, operating expense, initial investment.

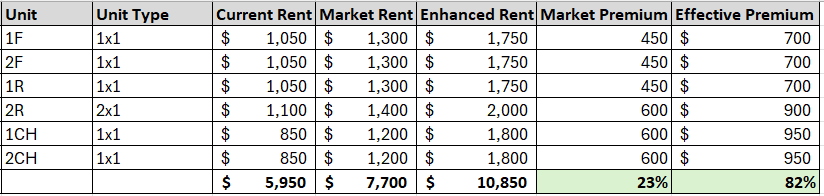

On the expense side, we can keep the numbers the same as our assumptions. However, the revenue needed to be revised lower to match the true bedroom counts of the two coach house apartments.

Updating the rent alone reduced the 5-year rate of return by 2% to 12%.

The biggest issue is the physical state of the property and the initial investment required to bring it up to the premium rent. And even then, there are definitely questions about whether or not it is physically possible to do those things. For example, adding in central ac would reduce the already small apartment size (if there is room to put it), adding 2 additional water heaters may require additional structural plumbing changes to separate out the different units, etc.

But even if it were possible, an initial investment of $100k minimum would be required to renovate it to achieve desired rents. We also can’t forget to factor in additional vacancy costs as the time to do these improvements would require concessions and/or more vacancies for other units.

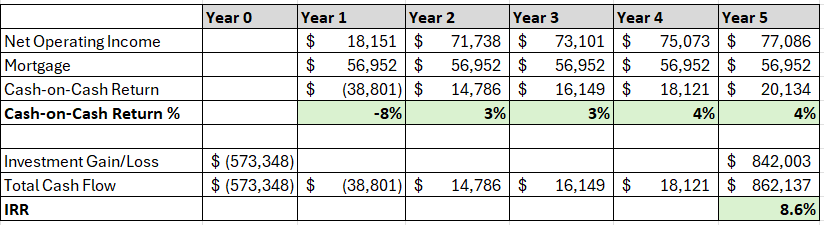

The final 5-year rate of return, if purchased at the $989k list price, would be <9%.

Conclusion

Ultimately, this property did not meet the cash flow and overall ROI that we are looking for, so we decided not to put in an offer. It’s true that we could’ve submitted an offer below $900k to offset the required initial investment for improvements. Even then, there was still a lot of risk just to hit low double-digit return numbers. Typically, if I’m investing in something below 13% in projected annual return, it needs to come with little risk. This was not that case.

Disclaimer: This is not financial advice. This content is for educational purposes only. Use your own judgement for your investing decisions.

Have a question or thought about my analysis? Feel free to add a comment below.